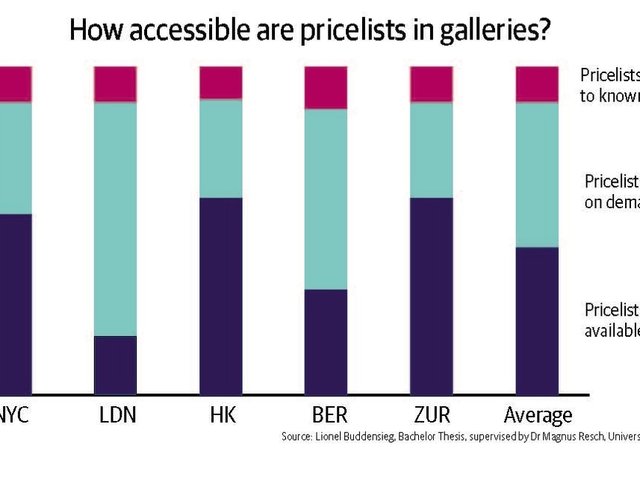

A Twitterstorm erupted in the US last month over the findings of survey of 8,000 art galleries based in the US, UK and Germany. Cultural researcher and Larry’s List co-founder Magnus Resch found (no surprise here for those in the know) that running an art gallery is tough, with more than half turning over less than $200,000 a year and 30% running in the red.

It’s his solutions, many of them classic business techniques, that have whipped upthe debate. None more so than the suggestion that most artists should be paid only 30% of sales not the traditional 50/50 split of most galleries (superstar artists aside).

It probably hasn’t helped that he divides artists into some all-too-pithy categories: Poor Dogs (don’t make money, take up heaps of gallery cash and staff time), Question Marks (future greats or future poor dogs), Stars (self-explanatory), and Cash Cows (generate a lot of money but seen in the art world as “too commercial”). While all of us know exactly what Resch means, it’s not often that you see it in print.

—Jane Morris

Magnus Resch Author of Management of Art Galleries, co-founder of the art collector database Larry’s List and Professor of Art Management at the University of St Gallen, Switzerland

I strongly believe that art galleries are the most important intermediaries in the art market. So, setting aside the handful of extravagantly successful ones, why do so few thrive? A simple economic analysis should make any potential gallerist pause to think; it is a textbook inefficient market, with too much supply meeting too little demand. But a further problem is found in the practices of the gallerists themselves; they have never changed their business model, relying on white walls, commissioned art, underpaid (or unpaid) interns, identikit opening events, 50/50 artist deals, and a presence at fairs. While art can be innovative, the business surrounding it is not.

It’s time for a change because the challenges of running a gallery have increased, with exorbitant rents, rising art fair costs, international competition, private sales by artists, artist poaching by ubergalleries, and auction houses now eating into traditional gallery business. The headline result is dramatic: one-third of all galleries operate in the red.

If galleries are to survive, they must rethink their business practices. I’m not the smart guy with all the answers, but I did analyse businesses from all over the world to identify the success factors. Notably, flourishing galleries (and not only the big ones with a Sotheby’s-like salesforce) exploit the secondary market to create strong revenue streams that cross-finance the capital and time invested in building up artists in the primary market. Growing with the artist is all very romantic. But if your rising star should fall by the wayside, you die. So you would do better to diversify from the start.

Flexibility is the second rule of the game. Why would you treat all artists the same? A young emerging artist gets the same 50% as the gallery’s superstar artist. Wait a moment! A gallerist covers far more risk by building up the young artist—and should be rewarded for this, taking a higher share. The same flexibility should be applied to the superstar. If you don’t want to see him leaving to a larger gallery, offer more money.

Every year, people open galleries. I’m an entrepreneur myself, and I admire those who take a risk and just do it. However, too many wander completely unprepared into this venture. It’s not enough to be a great curator. In today’s gallery world you need to be a real estate agent, a lawyer, a politician (to get into fairs), a marketing genius, a salesperson, and a visionary. Or, be a true idealist: forget all I just told you, and do it for the love of the art.

Edward Winkleman Co-owner of Winkleman Gallery, New York, co-founder of the Moving Image art fair and author of How to Start and Run a Commercial Art Gallery (Allworth, 2009)

As much as many young artists—and their friends and families—feel the traditional 50/50 commission split between artist and gallery is ripping the artist off (“The mafia only takes 30%,” I've been told), the truth of the matter is it’s the gallery who most frequently gets the short end of that stick. At least in the beginning.

The rationale behind the 50/50 split with emerging artists has never been about economics. What it costs most galleries to promote an unknown artist in a single solo exhibition, ongoing online and back-office presence, and a few art fairs, far exceeds the amount of money they will likely make from selling the average number of works at the emerging artist price points over the course of the first year or two. It's only by taking a long-term view that most dealers can recoup their investment in promoting most emerging artists, even when taking 50% of any sales. The rationale behind the 50/50 split has therefore been more symbolic of an earnest partnership, a collaboration between equals, with the goal of convincing the artist to stick around long enough for their prices to rise to where the dealer can feasibly see a reasonable return on their investment.

One of the conclusions I come to in my new book is that many emerging and mid-level galleries are too soon rushing into representation agreements with emerging artists (leading to far too many of them dropping more artists than they have poached from their rosters, creating a justified air of mistrust between artists and dealers). The suggestion Magnus Resch makes that dealers create a laboratory-style context for presenting and testing out new artists before offering them representation makes a great deal of sense to me. I found Resch’s book an important addition to the coming tidal wave of transparency approaching the art market, whether it's ready for it or not.

Resch’s argument that in the less expensive, less high-profile “garage” or “laboratory” context it makes sense to pay unrepresented artists less than 50% of any sales, however, does not take account of the symbolism of the traditional 50/50 split. Sure, the unrepresented artist understands they are not entering into a full-time collaboration between equals, but even that context is problematic because it is likely to create resentment. Sure, dealers can explain the economics to artists (just be prepared for retorts about studio rents, production costs, mountains of unpaid student loans, etc.), but to my mind it's sending the message that the artist should be grateful for this opportunity, rather than the more encouraging message that the gallery feels what the artist is doing is interesting or important. The 50/50 split underscores that message, emphasizing the nurturing role every gallery working with emerging artists should play.

Edward Winkleman’s forthcoming book, Selling Contemporary Art: How to Navigate the Evolving Market, is published by Allworth.

William Powhida Artist

There’s not much light at the end of this tunnel however you split the sales. The art market is supported by a handful of wealthy collectors and, although increasingly higher sums are being spent on individual works of art, the market as a whole is actually shrinking as fewer people accumulate more wealth. The choices of the super rich are both exceedingly expensive and also quite narrow as sales concentrate at the top end of the art market. According to an Artsy editorial on the TEFAF 2014 market report, just 0.5% of sales accounted for 48% of the art market that year. This proportion reflects the overall distribution of sales in the art market’s star system and reveals what we already know: very few dealers or artists make much money.

Here’s why Resch’s 70/30 proposal, even out of context, is so awful: we’ve created a profit-seeking industry around the sale of art that begins but rarely ends with the artist. Artists have no resale rights in the US, inconsistent fees, and little room to negotiate commercial leases for work space. All the big market operators, from Artsy to the art fairs, have figured out how to extract a percentage from the distribution of art, and every other creative industry has figured out how to share in residual income from reproduction and resale except for the visual arts.

Today most artists and dealers compete for a sliver of the primary market’s dragon’s tail: the long, thin spread of what is left over in the market after the blue chips take their sizeable cut. Resch’s suggestion that artists should share in even less of the value they create that supports a $51 bn industry and 2.8m jobs is frankly insulting. The enduring myth that artists aren’t in this for the money helps prevent us from advocating for our own interests and slows the work done by groups like W.A.G.E. and ASAP who need our support to lobby for artist fees, resale rights, and commercial lease rights in the fight for greater equity for artists, not less as Resch proposes. If Resch, the professor of “art marketing” and self-described “failed” start-up entrepreneur is offering suggestions, I think we as artists would benefit from making a few of our own after reading books like The Management of Art Galleries.

Sylvain Levy Collector of Chinese contemporary art, Paris

In his survey of art galleries, Resch suggests that: “Galleries should pay themselves more and artists less (70/30 in favour of the gallery).” This is a particularly provocative statement, possibly aimed at creating controversy and thus generating sales. As a solution to the difficulties of operating a gallery business, it does not go to the root of the problem, which is the economic model of a contemporary gallery. The issue is more about securing steady sales and then only diminishing costs. More and more collectors, especially new ones, are relying on “branded” galleries and artists for their purchases. Consequently, it is extremely important for galleries today to build a strong reputation and brand image, through which they can create a loyal client base of collectors who will buy established artists but also emerging artists. Galleries need to do this not only with a strong exhibition programme but also with additional events, physical presence at fairs, advertisements in magazines and savvy use of social media. That’s the only way for a gallery to keep their artists from going elsewh ere. In addition to trust, loyalty, and long-term relationships with artists and collectors are the key factors to success for a gallery.

Secondly, galleries need to really look at all their operational costs. In addition to the well-known cost of exorbitant rents in leading art hub cities such as London, New York and Paris, there is the huge cost of fair participation. All of these factors directly affect the economic viability of a gallery. As a result, before reducing artists’ salaries, a gallerist should consider other factors more carefully. Only take part in fairs where you can cover your expenses and move the location of your spaces to affordable locations. People visit galleries less and less and increasingly rely on jpegs to buy art so where you are located matters less than it ever has.

I fear that we’re entering an era where cultural goods are increasingly under-valued. With the exception of celebrity artists, those in the creative sector are generally paid far less than people working in other industries, be it finance, real estate, or sports. Cultural goods have intrinsic value, and this value has a price attached to it. The less artists are valued for their creativity, the less encouraged they will be to produce, and the fewer cultural goods will be left for posterity. Imagine a world without creativity, that would be the greatest cost to society.

Kenny Schachter Art dealer, curator, collector, and writer, London

The main premise of Resch’s book is that too many contemporary art galleries lose money and those that make it don’t make enough. Sounds like the daily dinner conversation with my wife. Resch sent a survey to 8,000 galleries in addition to operating three of his own in furtherance of his research (though there are no details of his own experiences included). The statistics he cites to illustrate his primary thesis that galleries are lousy at business include the revelation that fully 30% of the respondents actually lose money yearly. This confirms my long held belief that gallerists are among the kindest, most altruistic lot on the face of the earth: dealers do it for free! Would make a good giveaway bumper sticker (read on).

Don’t be afraid of red, yellow and blue (as Barnett Newman would say) or of management consultants. The suggestion that art dealers should embrace standard techniques of the business world is slightly misguided as the art world is its own universe with its own language and particular way of doing deals. I agree with the premise that art dealers generally display a weakness when it comes to number crunching and could benefit from more acumen with figures other than nudes—but hey, we don’t do much math other than applying discounts (albeit with hesitation). Anyway, art is not reducible to a series of MBA formulae like CARG (compound annual growth rate), speaking of which, how was yours Magnus during your run of gallery proprietorships?

A surprising finding is that galleries put their own artists above auction houses as perceived threats to their business models. After 25 years of working with artists of all stripes I’m glad I’m not alone in complaining about having the oxygen sucked out of my mouth by some recent art graduate who believes he or she has the power to cure humanity of a social ill. Resch recommends representing fewer artists, taking bigger gallery commissions and cutting loose the “dogs”. In his view, then, a sure-fire route to success is to rid the gallery of the artists that constitute the foundation of the business (or pay them less). But when viewed as a competitive threat, it makes perfect sense.

Resch says sales should be celebrated to buttress the business: can’t argue with that, I heard Gagosian books the Folies Bergère every time a big client rolls into town. He also proposes giveaways such as free doodads, tokens and souvenirs designed by artists, without doubt a way to staunch hemorrhaging losses. He also suggests letting your clients get involved in the actual making of the art…obviously allowing collectors to make your art for you is a telltale sign of a fine, fine artist. Happy hour discounts, now there’s a plan: piña colada with your Picasso?

The strength of the book is its case studies of dealers, including Jeanne Greenberg, Per Skarstedt, Vanessa Carlos, and others, though the stories do little to confirm or disprove Resch’s theories about a dire lack of structural management practices. The successes vividly depict that there is not a single quick fix or rote plan to make it in the trade instead, tenacity is the common thread. Ticking all the business school boxes in the world won’t make up for determination and hard work. That and a few good eyes should do it.

If you take Management of Art Galleries with humour and a 100 grains of salt you may find yourself enjoying a chuckle while taking in a handful of fun facts and studies that do no more than scratch the surface of the art market’s realities. But what more could you want from this little day-glo book? I need a management consultant pronto; can someone make me a graph please?